![]()

2016-FRR Dumps Special Discount for limited time Try FOR FREE

2016-FRR Dumps for success in Actual Exam Nov-2023]

GARP 2016-FRR (Financial Risk and Regulation) exam is a comprehensive assessment of a candidate's knowledge and understanding of financial risk management and regulation. 2016-FRR exam is designed to test candidates' ability to identify, measure, and manage financial risks within an organization, as well as their understanding of regulatory frameworks and compliance requirements.

The FRR Series exam is available to individuals who have a minimum of two years of professional experience in risk management, regulation, or a related field. 2016-FRR exam is divided into two parts, with the first part covering foundations of risk management and the second part focusing on regulatory compliance. 2016-FRR exam is computer-based and consists of multiple-choice questions. Candidates are given four hours to complete each part of the exam. Upon successful completion of the exam, candidates are awarded the FRR Series Certification, which is recognized globally as a mark of excellence in financial risk management and regulatory compliance.

NEW QUESTION # 71

If the yield on the 3-month risk free bonds issued by the U.S government is 0.5%, and the 3-month LIBOR

rate is 2.5%, what is the TED spread?

- A. 0.5%

- B. -2.0%

- C. 3.0%

- D. 2.0%

Answer: D

NEW QUESTION # 72

When a credit risk manager analyzes default patterns in a specific neighborhood, she finds that defaults are

increasing as the stigma of default evaporates, and more borrowers default. This phenomenon constitutes

- A. Adverse selection

- B. Speculative bias

- C. Moral hazard

- D. Herd behavior

Answer: D

NEW QUESTION # 73

To estimate the interest charges on the loan, an analyst should use one of the following four formulas:

- A. Loan interest = Risk-free rate + Probability of default x Loss given default - Spread

- B. Loan interest = Risk-free rate + Probability of default x Loss given default + Spread

- C. Loan interest = Risk-free rate - Probability of default x Loss given default + Spread

- D. Loan interest = Risk-free rate - Probability of default x Loss given default - Spread

Answer: B

NEW QUESTION # 74

Rising TED spread is typically a sign of increase in what type of risk among large banks?

I. Credit risk

II. Market risk

III. Liquidity risk

IV. Operational risk

- A. I only

- B. I and IV

- C. I, II, and III

- D. II only

Answer: A

NEW QUESTION # 75

Sam has hedged a portfolio of bonds against a small parallel shift in the yield curve using the duration

measure. What should Sam do to ensure that the portfolio is hedged against larger parallel shifts in the yield

curve?

- A. Since the portfolio is duration hedged Sam does not need to take additional positions.

- B. Take positions to increase the duration

- C. Take positions to reduce the duration

- D. Take positions to make the convexity zero

Answer: D

NEW QUESTION # 76

For a bank a 1-year VaR of USD 10 million at 95% confidence level means that:

- A. There is a 5% chance that the worst loss would be USD 10 million in a year.

- B. There is a 5% chance that the bank would lose more than USD 10 million in a year.

- C. There is a 5% chance that the bank would lose less than USD 10 million in a year.

- D. There is a 5% chance that the least loss would be USD 10 million in a year.

Answer: B

NEW QUESTION # 77

Which one of the following statements correctly identifies risks in foreign exchange forwards?

- A. Long-term forward price fluctuations are driven by changes in the spot exchange rate, since most

inter-country interest rates differentials are small, and the effect of compounding is large for short

periods of time. - B. Long-term forward price fluctuations are driven by changes in the spot exchange rate, since most

inter-country interest rates differentials are significant, and the effect of compounding is small for short

periods of time. - C. Short-term forward price fluctuations are driven by changes in the spot exchange rate, since most

inter-country interest rates differentials are significant, and the effect of compounding is large for short

periods of time. - D. Short-term forward price fluctuations are driven by changes in the spot exchange rate, since most

inter-country interest rates differentials are small, and the effect of compounding is small for short

periods of time.

Answer: D

NEW QUESTION # 78

Which of the following statements about endogenous and external types of liquidity are accurate?

I. Endogenous liquidity is the liquidity inherent in the bank's assets themselves.

II. External liquidity is the liquidity provided by the bank's liquidity structure to fund its assets and maturing

liabilities.

III. External liquidity is the non-contractual and contingent capital supplied by investors to support the bank in

times of liquidity stress.

IV. Endogenous liquidity is the same as funding liquidity.

- A. II, III

- B. I, III

- C. I, II

- D. I, II, IV

Answer: B

NEW QUESTION # 79

Which one of the following four option types has two strike prices?

- A. Range options

- B. Shout options

- C. American options

- D. Asian options

Answer: B

NEW QUESTION # 80

From the bank's point of view, repricing the retail debt portfolio will introduce risks of fluctuations in:

I. Duration

II. Loss given default

III. Interest rates

IV. Bank spreads

- A. I

- B. III, IV

- C. I, II

- D. II

Answer: B

NEW QUESTION # 81

Bank Muri has $4 million in cash and $5 million in loans coming due tomorrow with an expected default rate

of 1%. The proceeds will be deposited overnight. The bank owes $ 9 million on a securities purchase that

settles in two days and pays off $8 million in commercial paper in three days that is not expected to renew. On

day 2, $1 million in loans is coming in with an expected default rate of 1% and on day 3, $2 million in loans is

coming in with expected default rate of 2%. How much should the bank plan to raise in order to avoid liquidity

problems?

- A. $508 million

- B. $510 million

- C. $500 million

- D. $550 million

Answer: B

NEW QUESTION # 82

A customer of EtaBank, Alfred Fall, fell on the marble floors of the bank and sustained substantial injuries.

Subsequently, he won a personal injury claim of $50,000 against EtaBank. How should EtaBank's operational

loss data event information database categorize this event?

- A. This event would qualify as "Employment Practices and Workplace Safety".

- B. This event would not qualify as an operational risk event.

- C. This event would qualify as "Legal Risk".

- D. This event would qualify as "Business Disruption and System Failures".

Answer: A

NEW QUESTION # 83

What do option deltas measure?

- A. The rate of change of the option value with respect to changes in the price of the underlying instrument.

- B. The rate of change of the option value with respect to changes in volatility of the underlying instrument.

- C. The sensitivity of the option value to changes risk free interest rate.

- D. The sensitivity of the option value to the passage of time.

Answer: A

NEW QUESTION # 84

Which of the following are among the main uses of risk reports?

I. Identification of exceptional situations that require managerial attention.

II. Display the relative risk among different trades.

III. Specify how RAROC will be maximized within the bank.

IV. Estimate the overall risk levels of the bank.

- A. II, III, and IV

- B. II and IV

- C. I, II and IV

- D. II and III

Answer: C

NEW QUESTION # 85

Which one of the following statements is an advantage of using implied volatility as an input when calculating

VaR?

- A. Implied volatility assumes volatilities are constant which makes it easy to implement in models.

- B. Current market data is used to determine implied volatilities, which makes them forward looking

measures - C. Loss probabilities from the standard normal distribution are used to compute implied volatilities, which

makes it easy to compute the. - D. Implied volatilities are better at predicting actual volatilities

Answer: B

NEW QUESTION # 86

Which one of the following four statements about equity indices is INCORRECT?

- A. Capitalization-weighted equity indices are not generally considered better to track the performance of an

overall market. - B. Price-weighted equity indices give greater weight to shares trading at high prices.

- C. Equity indices are numerical calculations that reflect the performance of hypothetical equity portfolios.

- D. Equity indices do not trade in cash form, rather, they are meant to track the overall performance of an

equity market.

Answer: A

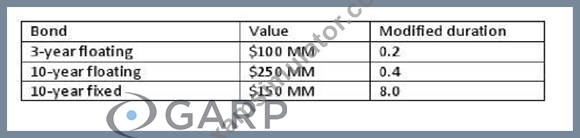

NEW QUESTION # 87

A portfolio consists of two floating rate bonds and one fixed rate bond.

Based on the information below, modified duration of this portfolio is

- A. 4.44

- B. 3.00

- C. 2.64

- D. 4.28

Answer: C

NEW QUESTION # 88

What is a difference between currency swaps and interest rate swaps?

- A. Currency swaps do not require the exchange of notional principal on maturity.

- B. Currency swaps are OTC derivative contracts.

- C. Currency swaps allow banks and customers to obtain the risk/reward profile of long-term interest rates

without having to use long-term funding. - D. Currency swaps generate foreign exchange rate risk in addition to interest rate risk.

Answer: D

NEW QUESTION # 89

To improve the culture and awareness of the operational risk, Gamma Bank's CRO decides to promote three

activities within her organization. Which one of the following four activities is NOT typically used to develop

an operational risk framework?

- A. Planning

- B. Marketing

- C. Training

- D. Auditing

Answer: D

NEW QUESTION # 90

Alpha Bank determined that Delta Industrial Machinery Corporation has 2% change of default on a one-year

no-payment of USD $1 million, including interest and principal repayment. The bank charges 3% interest rate

spread to firms in the machinery industry, and the risk-free interest rate is 6%. Alpha Bank receives both

interest and principal payments once at the end the year. Delta can only default at the end of the year. If Delta

defaults, the bank expects to lose 50% of its promised payment.

What may happen to the Delta's initial credit parameter and the value of its loan if the machinery industry

experiences adverse structural changes?

- A. Probability of default and loss at default may increase simultaneously, while duration rises causing the

loan value to decrease. - B. Probability of default and loss at default may decrease simultaneously, while duration rises causing the

loan value to decrease. - C. Probability of default and loss at default may decrease simultaneously, while duration falls causing the

loan value to decrease. - D. Probability of default and loss at default may increase simultaneously, while duration falls causing the

loan value to decrease.

Answer: D

NEW QUESTION # 91

To ensure good risk management which of the following should be true about the CRO role and function?

- A. The CRO should receive compensation that is directly determined by the profit of the trading desk.

- B. The CRO should report to the CEO or the Board of Directors.

- C. The CRO should not be involved with the setting of risk limits.

- D. To ensure efficient flow of information the CRO should not be independent of business units.

Answer: B

NEW QUESTION # 92

10 basis points are equal to:

- A. 1%

- B. 0.01%

- C. 0.1%

- D. 10%

Answer: C

NEW QUESTION # 93

Which one of the following statements accurately describes market risk tolerance?

- A. Market risk tolerance is the maximum loss the bank is willing to bear due to fluctuations in market

prices and rates. - B. Market risk tolerance is the minimum loss the bank is willing to bear due to fluctuations in market prices

and rates. - C. Market risk tolerance is the maximum likely gain in the market value of portfolios over a given period

of time. - D. Market risk tolerance is the maximum loss in the market value of financial instruments caused by the

failure of the counterparty to meet its obligations.

Answer: A

NEW QUESTION # 94

......

GARP 2016-FRR Certification Exam is a computer-based exam that consists of 100 multiple-choice questions. Candidates have four hours to complete the exam. 2016-FRR exam is offered in English and can be taken at various testing centers around the world. The passing score for the exam is 70%.

Accurate 2016-FRR Answers 365 Days Free Updates: https://www.itexamsimulator.com/2016-FRR-brain-dumps.html

Realistic 2016-FRR 100% Pass Guaranteed Download Exam Q&A: https://drive.google.com/open?id=1DWTu0TNAltHfUqxxnIr5Em6jCYlS0oNu